A Tale of Two Strategies: Remain Independent or Join a System

Since the beginning of the COVID-19 pandemic, the trend of independent hospitals and small community health systems joining larger systems via full-asset mergers has slowed when compared to the last 10 years overall. While the number of announced transactions for 2023 (55) is up from 2022’s recent historic low (52), it still trails the nearly 100 transactions announced each year from 2012 to 2019.

Despite a decrease in the total number of transactions, the average size of each deal has notably increased in recent years, indicating that the types of organizations being acquired by larger systems are not the small, independent hospitals of 10-plus years ago. Rather, faced with sky-high labor costs and competitive pressure stemming from nontraditional organizations investing in the healthcare space, midsize community systems—which previously had large enough balance sheets to weather economic uncertainty—are now pursuing partnerships with larger systems as their strategic direction of choice¹.

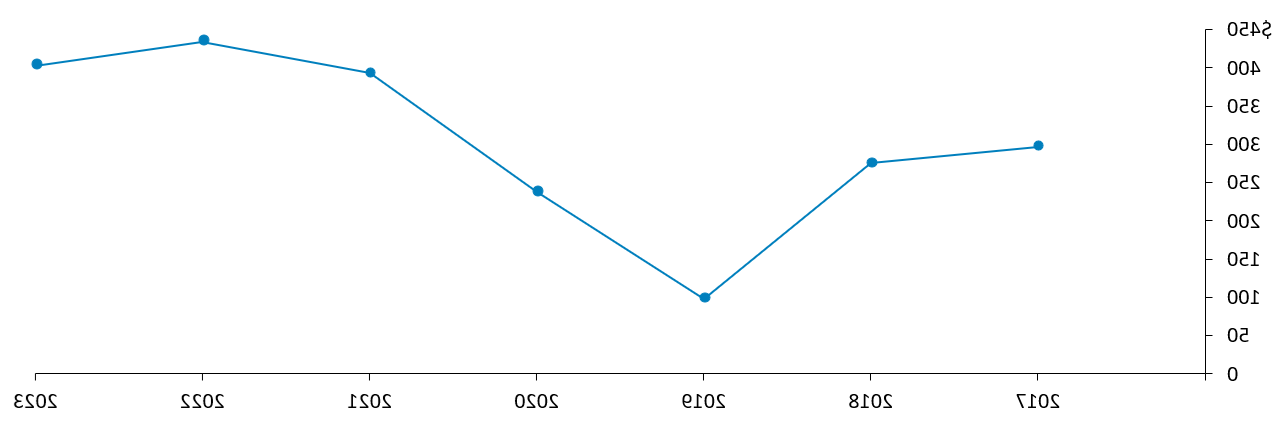

The average size of the hospitals engaging in transactions has grown in recent years, with the average revenue of transacting facilities exceeding $400 million. As shown in figure 1, this surpasses the prepandemic historic high of $296 million². For large, well-financed institutions, the current market represents a buyer’s opportunity as midsize systems and the remaining independent hospitals express significant concern about taking on the future alone.

FIGURE 1: Revenue per Selling Hospital, 2017–2023 (in millions)

There are various benefits smaller systems hope to realize in joining larger systems, including:

- Infrastructure to help manage a shifting payer environment.

- Expertise in developing ambulatory care sites.

- Access to capital at affordable rates.

- Support to address rising labor costs.

- Increased market access.

- The ability for programmatic and physician growth.

However, giving up community-based governance to join a system is not a sacrifice any entity makes without much deliberation and contemplation. To support this decision-making, leaders typically compare the contrasting futures of remaining independent versus joining a larger system. Detailed below are the key success factors to be considered by boards and executives as they determine which strategic direction to pursue.

Achieving Success When Remaining Independent

If an organization decides to remain independent, its future success depends on the eight factors shown below. Community health systems that are positioned strongly in these eight areas are likely well positioned to remain independent, while those that are not should consider other options³. Moreover, the value gained from joining a system will be far less for well-performing systems compared to those in weaker positions.

It’s important to note that the ability of an organization to actually control or impact each factor varies. System leaders should carefully analyze their position relative to each factor and create strategies to strengthen those that can be influenced.

FIGURE 2: Factors Determining Success of Remaining Independent

- Geography: Both broader geographic coverage and long distances to other competitors offer a strong advantage to the community systems that enjoy them. While an organization’s location may be difficult to change, service area coverage can be improved with careful planning and targeted physician partnerships.

- Physician Alignment: Aligning physicians under three key elements—economics, clinical activity, and purpose—is essential to strong physician-hospital relationships. Because physicians influence all parts of the care continuum’s growth and effectiveness, strong physician alignment is the top indicator of success. Moreover, it can be directly impacted by leadership via targeted initiatives.

- Payer Relationship: The payer mix of a given community plays a large part in determining the financial resources available to hospitals. Markets with large concentrations of payers or high percentages of lower-reimbursing payers have a large risk and low margin for error. Additionally, systems that have not developed the relationships and infrastructure necessary to manage risk-based payments are facing significant challenges in the future payment environment.

- Cost and Revenue Structure: Those that have dramatically reduced overhead and, through partnerships, optimized economies of scale outside their organization have strengthened their financial position and thereby their ability to remain independent. A larger system will not offer much by way of cost savings.

- High-Quality Inputs, Processes, and Outcomes: Providing high-quality care is almost entirely within an organization’s sphere of influence. Leadership’s role in defining the quality signature of the organization has become increasingly important as consumers demand more transparency. Moreover, creating a high-quality signature in the market can be difficult for competitors to emulate, as it requires coordination and cooperation with various stakeholders, most notably physicians.

- Capital Asset Base: Organizations that have not advanced their facilities and technologies, or those with a poor balance sheet position, are likely to face challenges if they remain independent of a larger system. The future environment will demand financial flexibility and access to capital at affordable rates.

- Community Support: A community’s commitment to supporting a hospital’s independence is directly correlated to the perceived value provided by the facility. An organization’s strong ties to the community can reduce opportunities for competition from physicians or outside players and, in some cases, directly support its financial success through tax revenues or philanthropy.

- Continuum Management: Being an integral part of its community’s continuum of care has always been important for a hospital’s continued success. But with the increasing emphasis on population health, an organization’s ability to lead and manage the continuum of care beyond the acute care component offers it a strong and durable competitive advantage over other organizations in the market.

Achieving Success When Joining a System

Organizations that choose to join a larger system must follow up that decision with two critical next steps: (1) maximize their value to put them in the strongest bargaining position and (2) pick the right partner.

In some cases, picking a partner is straightforward. For instance, some hospitals that join large regional systems do so because nearly their entire medical staff is already employed by the system. As such, there are no other realistic options.

In other cases, however, the organization must determine the right system partner using the criteria below.

Mission, Vision, Values, and Culture

Joining a system with a significantly different mission, vision, set of values, or culture is a difficult proposition, and leaders must honestly and realistically assess the impact of these differences. This is especially true when a nonprofit entity considers a for-profit partner. In these scenarios, the statement “culture trumps strategy” should drive decision-making.

Governance

Systems today are continually moving toward a more centralized model in response to industry pressures. While the governance consideration often revolves around reserve powers, the real priority for community systems should be determining how a locally based, managed, and governed institution will remain in touch with its population’s needs under this centralization and how future decision-making structures will allow for these needs to be met (e.g., through the remaining structures of the local board).

Management and Structures

As mentioned above, systems are rapidly consolidating decision-making, which means the role and structure of local management must be considered when seeking a partner. For example, will the local management team be able to lead initiatives for the community, or will its role be simply implementing and managing decisions from the system office? Additional elements to be examined include (1) the potential centralization of key services, such as finance, purchasing, and IT; (2) changes to key reporting relationships for physicians and staff; and (3) any shifts in the ownership of decision-making related to strategic and capital investments.

Additionally, strong consideration should be given to the system’s ability to streamline processes, especially back-office processes that are sensitive to scale economies. More value must be created to offset the overhead assignments from corporate offices that are a reality of every system.

Continuum of Clinical Services

A primary driver of acquisitions and system growth is the focus on ambulatory health models and the changing healthcare delivery paradigm that many smaller community systems feel ill-prepared to handle. As such, the potential partner’s positioning within the continuum, as well as the ability to organize and provide value across it, should be evaluated.

Finances

Finances tend to be the central focus of many partnership and merger discussions. Organizations joining a larger system generally work to secure the best financial payouts possible for their community and/or the strongest commitments of capital investment for the local healthcare delivery system. Typical agreements have moved away from the “replacement hospital” pledges seen a few years ago to now include targeted inpatient facility upgrades and investments in physicians, ambulatory spaces, and other parts of the healthcare continuum.

Looking to the Future

Macroeconomic and regulatory changes have shifted the competitive landscape for community hospitals and smaller, regional healthcare systems. Responding appropriately to these changes means determining the best strategic direction forward for your organization, whether it be remaining independent or joining a larger system. While obviously no one knows what the future holds, leaders can consider a variety of factors to help assess their organization’s potential for success under each scenario. Organizations that fail to capitalize on the success factors within their control risk being left behind by potential partners or forced to respond reactively to the strategic initiatives of better prepared systems.

Learn More About our Perspective on Market Consolidation

¹ Jared Langus, Mark Johnston, Brian Barnthouse, Sean O’Donovan, Henry Strull, Andrew Schroeder, Vasco Zamudio Estatuet, Lucas Hein. Healthcare M&A Quarterly Update: Q2 2024. July 2024.

² LevinPro Healthcare M&A. http://accounts.levinassociates.com/login/index

³ Jeff Hoffman, Jared Langus, Mark Johnston. Identifying the Most Responsible Moment for Partnerships and Affiliations. ECG Management Consultants, May 2024. http://i0y.dos5.net/insights/article/3251/identifying-the-most-responsible-moment-for-partnerships-and-affiliations

Edited by: Emily Johnson

This article was originally published in the American Health Law Association Journal in July 25, 2024.

Copyright 2024, American Health Law Association, Washington, DC. Reprint permission granted.

Published August 2, 2024

You Might Also Like